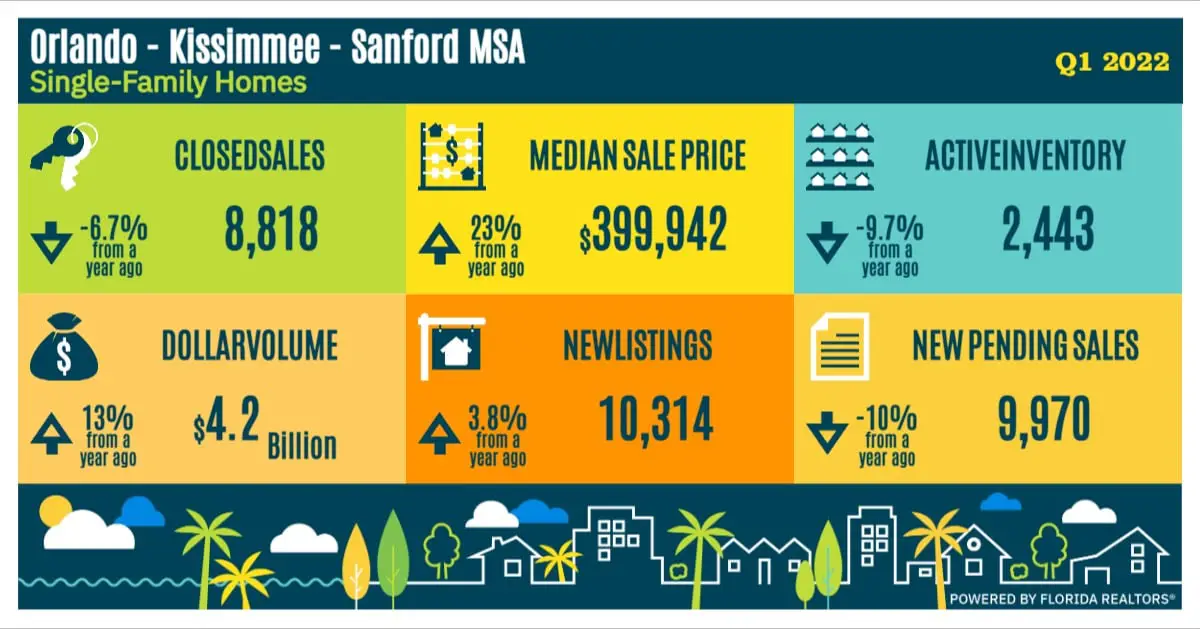

For the first quarter 2022, the Orlando – Kissimmee – Sanford metro area still remains fairly strong but appears to be in a transitional state with declining single-family home sales and increasing prices.

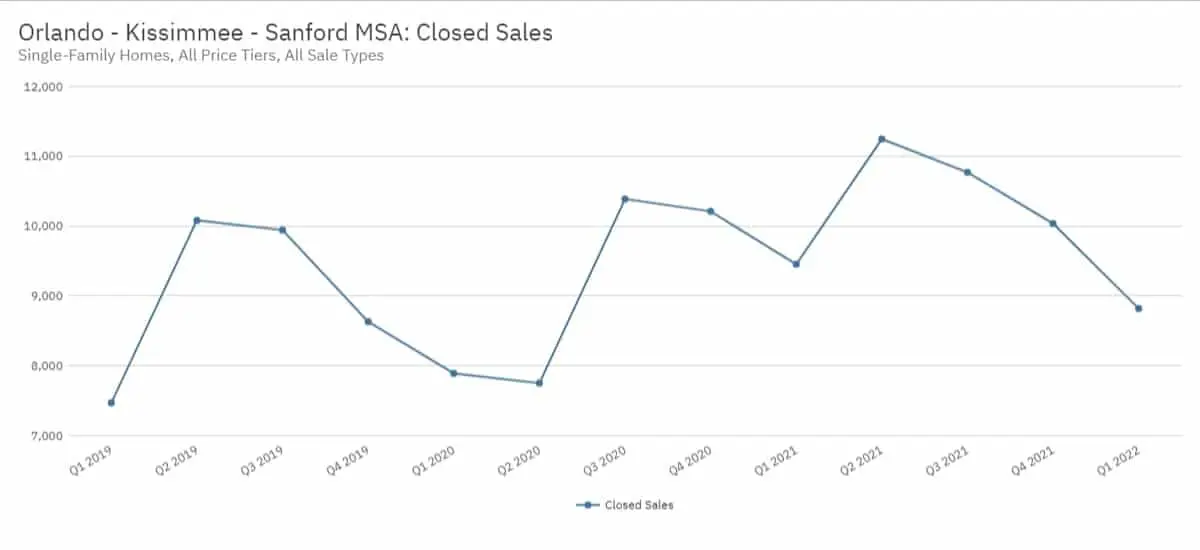

According to FloridaRealtors, there were a total of 8,818 existing single-family home sales throughout the greater Orlando area during the first quarter 2022. This represents a 6.7% decline from the number of existing single-family sale transactions during the first quarter 2021 (9,453).

The number of closed sales have declined over the past two quarters and are indicated to be as follows:

- Q1 2022 – 8,818 (down 6.7% year-over-year)

- Q4 2021 – 10,036 (down 1.7% year-over-year)

- Q3 2021 – 10,770 (up 4.4% year-over-year)

- Q2 2021 – 11,247 (up 45.1% year-over-year)

- Q1 2021 – 9,453 (up 19.8% year-over-year)

- Q4 2020 – 10,211 (up 18.3% year-over-year)

Based on the current level of activity, it is anticipated that the number of overall sales of existing single-family homes will continue to decline due to limited inventory levels, rising interest rates and record high home prices.

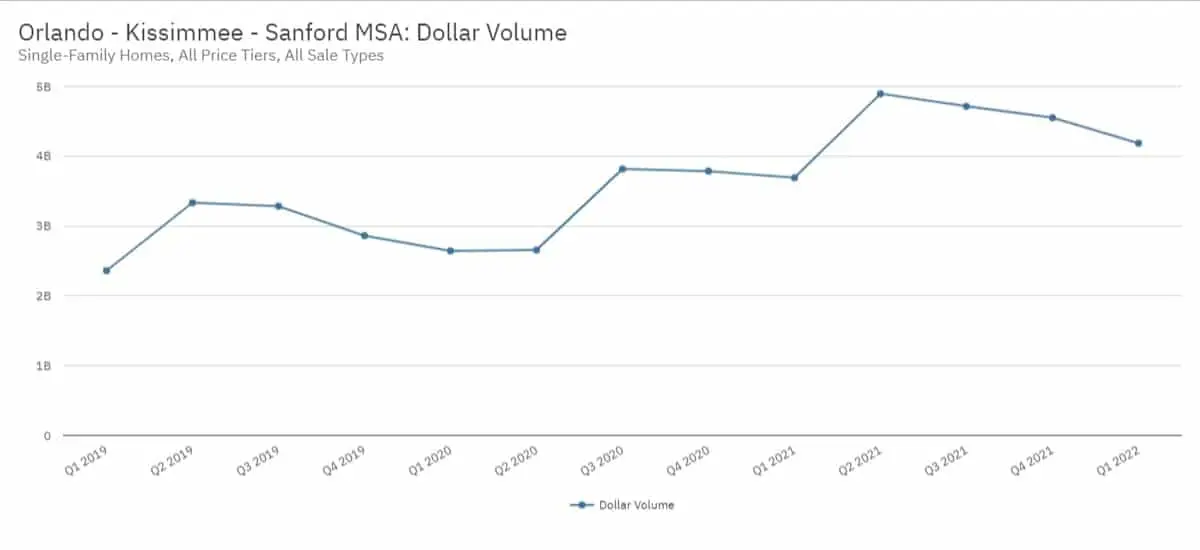

Overall dollar sales volume during the first quarter 2022 was $4.2 billion which is up by 13.4% on year-over-year basis from $3.7 billion. It should be noted, however, this is down from the second quarter 2021 amount of $4.9 billion.

- Q1 2022 – $4.2 billion (up 13.4% year-over-year)

- Q4 2021 – $4.6 billion (up 20.2% year-over-year)

- Q3 2021 – $4.7 billion (up 23.5% year-over-year)

- Q2 2021 – $4.9 billion (up 84.3% year-over-year)

- Q1 2021 – $3.7 billion (up 39.6% year-over-year)

- Q4 2020 – $3.8 billion (up 32.3% year-over-year)

Single Family Home Sale Prices (First Quarter 2022)

The median sale price is one of the preferred statistical methods for measuring price activity as it is not as sensitive of extraordinary high or low sale prices (that are not typical of a particular market area) which can easily skew the values.

For the first quarter 2022, the median sale price for existing single-family home sale transactions in the Orlando metro area was $399,942 which is 23.1% higher than that observed for during the first quarter 2021.

- Q1 2022 – $399,942 (up 23.1% year-over-year)

- Q4 2021 – $380,000 (up 20.6% year-over-year)

- Q3 2021 – $365,000 (up 17.7% year-over-year)

- Q2 2021 – $352,667 (up 19.1% year-over-year)

- Q1 2021 – $325,000 (up 14% year-over-year)

- Q4 2020 – $315,000 (up 12.5%% year-over-year)

For the same period, the average sale price for single-family home sale transactions in the Orlando – Kissimmee – Sanford metro area was $4747,799. This amount is 21.6% higher than the first quarter 2021 and largely driven by the 28.4% increase in the sale of homes over $1,000,000.

- Q1 2022 – $474,799 (up 21.6% year-over-year)

- Q4 2021 – $453,545 (up 22.3% year-over-year)

- Q3 2021 – $437,848 (up 19.1% year-over-year)

- Q2 2021 – $435,189 (up 27.0% year-over-year)

- Q1 2021 – $390,544 (up 16.5% year-over-year)

- Q4 2020 – $370,910 (up 11.8% year-over-year)

The number of homes sold above $400,000 continue to grow year-over-year by more than double digits with the number home sales above $1 million growing by more than 28%.

Affordability is continuing to become an issue as appreciation is limited the amount of homes being offered for sale at prices below $300,000.

| Initial Listing Price Point | New Listings | % Change (YOY) |

| Less than $50,000 | 2 | -71.4% |

| $50,000 – $99,999 | 27 | -18.2% |

| $100,000 – $149,999 | 65 | -61.3% |

| $150,000 – $199,999 | 213 | -59.4% |

| $200,000 – $249,999 | 483 | -62.3% |

| $250,000 – $299,999 | 877 | -51.5% |

| $300,000 – $399,000 | 2,748 | -4.5% |

| $400,000 – $599,000 | 2,841 | 57.0% |

| $600,000 – $999,999 | 1,227 | 79.1% |

| $1 million or more | 335 | 28.4% |

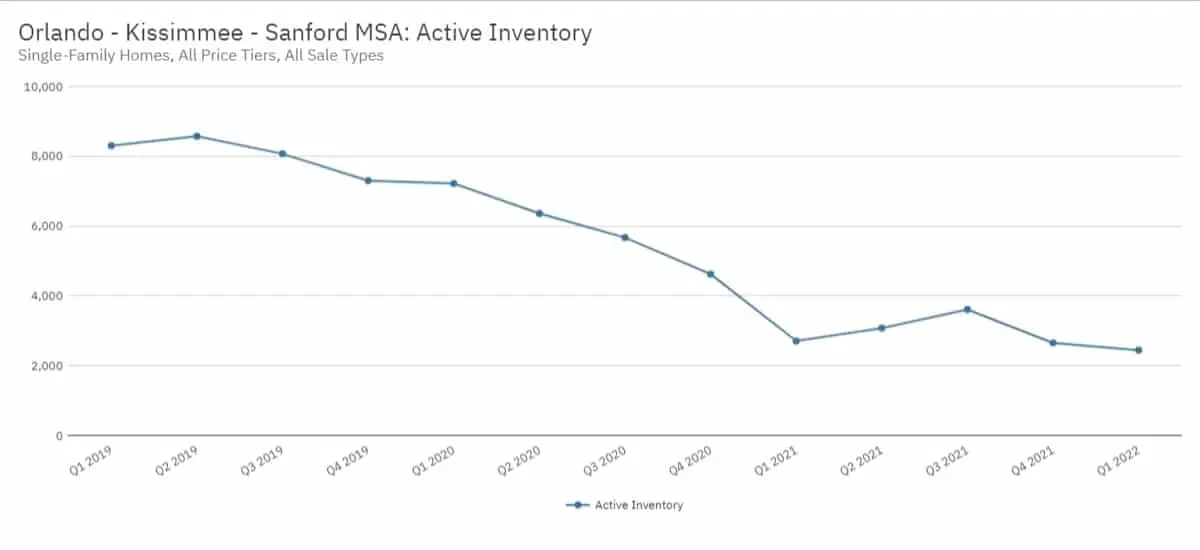

Single Family Home Inventory Levels (First Quarter 2022)

Inventory is the number of active property listings on the market for sale at any given point in time. This particular statistic is one of the main components in a healthy real estate market.

As of the end of the first quarter 2022, there were a staggeringly low 2,443 single-family homes available for sale throughout the greater Orlando area which is a 9.7% decline from the amount of inventory as of the end of first quarter 2021. In the past three years, overall inventory has been extraordinary low compared to historical levels as evidenced by 8,302 homes available for sale in the first quarter 2019.

- Q1 2022 – 2,443 homes (down 9.7% year-over-year)

- Q4 2021 – 2,650 homes (down 42.7% year-over-year)

- Q3 2021 – 3,610 homes (down 36.3% year-over-year)

- Q2 2021 – 3,075 homes (down 51.7% year-over-year)

- Q1 2021 – 2,706 homes (down 62.5% year-over-year)

- Q4 2020 – 4,623 homes (down 36.7% year-over-year)

The months supply of single-family home inventory as of first quarter 2022 was also historically low. At the current pace of sales, there is less than one month of inventory available for sale in the Orlando – Kissimmee – Sanford metro area which is down by more than 22% year-over-year.

- Q1 2022 – 0.7 months supply (down 22.2% year-over-year)

- Q4 2021 – 0.8 months supply (down 46.7% year-over-year)

- Q3 2021 – 1.0 months supply (down 50% year-over-year)

- Q2 2021 – 0.9 months supply (down 59.1% year-over-year)

- Q1 2021 – 0.9 months supply (down 62.5% year-over-year)

- Q4 2020 – 1.5 months supply (down 37.5% year-over-year)

Overall inventory is down substantially – the number of single-family home listings were new to the market during the first quarter 2022 decreased by 9.7% (from the first quarter 2021).

- Q1 2022 – 2,443 homes (down 9.7% year-over-year)

- Q4 2021 – 2,650 homes (down 42.7% year-over-year)

- Q3 2021 – 3,610 homes (down 36.3% year-over-year)

- Q2 2021 – 3,075 homes (down 51.7% year-over-year)

- Q1 2021 – 2,706 homes (down 62.5% year-over-year)

- Q4 2020 – 4,623 homes (down 36.7% year-over-year)

Due to demand levels and low inventory, the number of new listings are increasingly higher price points continues to grow. Following is a table of new single-family listings at individual price points as of the end of the first quarter.

| Initial Listing Price Point | New Listings | % Change (YOY) |

| Less than $50,000 | 3 | -70.0% |

| $50,000 – $99,999 | 23 | -37.8% |

| $100,000 – $149,999 | 52 | -62.6% |

| $150,000 – $199,999 | 216 | -59.9% |

| $200,000 – $249,999 | 468 | -59.2% |

| $250,000 – $299,999 | 967 | -47.3% |

| $300,000 – $399,000 | 2,954 | -0.6% |

| $400,000 – $599,000 | 3,430 | 68.8% |

| $600,000 – $999,999 | 1,655 | 87.9% |

| $1 million or more | 546 | 56.0% |

As of the first quarter 2022, the following table will show the number of active property listings at individual price points.

| Current Listing Price Point | New Listings | % Change (YOY) |

| Less than $50,000 | 0 | -100.00% |

| $50,000 – $99,999 | 9 | -57.1% |

| $100,000 – $149,999 | 12 | -66.7% |

| $150,000 – $199,999 | 47 | -63.0% |

| $200,000 – $249,999 | 115 | -45.8% |

| $250,000 – $299,999 | 228 | -25.5% |

| $300,000 – $399,000 | 458 | -21.7% |

| $400,000 – $599,000 | 761 | 16.4% |

| $600,000 – $999,999 | 484 | 6.8% |

| $1 million or more | 329 | 5.8% |

Are you thinking of selling?

Based on the year-end 2021 data, the current state of the market is highly favorable for seller. If you are a homeowner and are considering selling your personal residence, vacation home or investment property, not may be the perfect time to do so.

Our team has assisted sellers not only throughout the state of Florida, but in most major markets nationwide. We take a highly methodical and deliberate approach when working with or clients and have specific strategies to help get the best value for the property.

Contact us at info@quantumcos.com or learn more by visiting our web site at www.QuantumRealtyAdvisors.com.

The information provided in this website was derived from sources deemed to be reliable to is not guaranteed or warranted. All information, content, and materials available on this site are for general informational purposes only.