Recent trends in the Florida real estate market have been significantly influenced by the property insurance sector. With its propensity for severe weather events, such as hurricanes, Florida presents unique challenges to insurers. This has resulted in escalating premiums for property insurance, putting financial pressure on homeowners and potential buyers.

The situation is compounded by the limited number of insurance companies willing to underwrite in a state that is prone to natural disasters. This scarcity of options has the potential to hinder real estate transactions, as adequate and affordable insurance coverage is a prerequisite for mortgage approval in many cases.

Moreover, the escalating costs and decreased availability of property insurance are not only affecting homeowners but are also becoming a critical factor for new buyers in the Florida market. Insurance premiums have surged as a result of insurers incurring substantial losses to frequent catastrophes, reports of rampant insurance fraud, and significant payouts to legal fees.

These dynamics are making it challenging for homebuyers to budget for the true cost of owning property in Florida, which may in turn impact the overall demand in the state’s real estate market.

As the Florida property insurance market faces ongoing distress, with some insurers leaving the market and others becoming insolvent, the government-run Citizens Property Insurance Corporation is increasingly becoming a key player as the insurer of last resort. This development may offer some relief to homeowners and buyers struggling to find coverage, but it also highlights the systemic issues within the private insurance market that require long-term solutions to stabilize both the insurance and real estate sectors in Florida.

Impact of Property Insurance on the Florida Real Estate Market

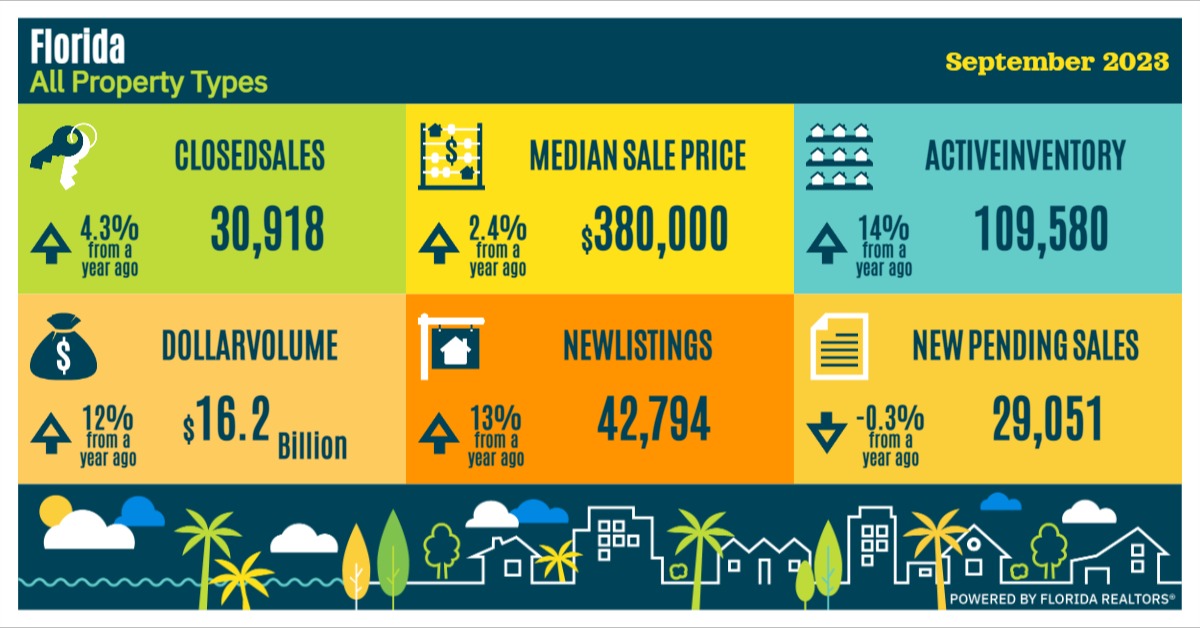

Florida’s real estate market is experiencing considerable disruption due to property insurance challenges, with significant effects on market value, sales, homeowner policies, and overall affordability.

Influence on Market Value and Sales

Florida’s property insurance crisis has had a measurable effect on the state’s real estate market. Climbing insurance costs, driven by natural disasters like Hurricane Ian, are directly impacting the market value of properties. Insurance availability and cost can deter potential buyers, slowing sales in the region.

Insufficient insurance coverage can also present a risk to investors, which reduces the attractiveness of Florida real estate as a safe investment opportunity.

Changes in Homeowner Policies and Coverage

Homeowners face changes in their insurance policies that impact their coverage. The insurance companies adapt to escalating risks by modifying the coverage options, often leading to reduced coverage scopes. These changes can include exclusions for certain types of damage, such as that caused by hurricanes, which are a significant threat in Florida.

The strategic response from insurers to mitigate risk exposure may involve tightening the underwriting criteria or completely withdrawing from high-risk areas, leaving fewer options for policyholders.

Insurance Rate Increases and Affordability

Rate increases in property insurance have significantly affected the affordability of owning a home in Florida. High-risk areas, particularly those prone to hurricanes, have seen insurance costs escalate, resulting in higher premiums for homeowners. These higher premiums contribute notably to the overall cost of insurance, which can be a considerable portion of a homeowner’s budget.

Attorney fees from insurance litigation represent a substantial portion of these costs, as noted by the Florida Office of Insurance Regulation, which in turn drives up premiums further. The steeper insurance prices may render homeownership unattainable for some, exacerbating affordability issues in the state’s real estate market.

Legislation and State Response

The Florida property insurance landscape is actively shaped by the interplay of legislation, governmental response, and judicial proceedings. These factors collectively influence the availability and affordability of property insurance.

Effects of Reinsurance on Rates

Reinsurance, which is insurance purchased by insurance companies to mitigate risk, deeply affects property insurance rates. Lawmakers and regulators work to stabilize the market and prevent rate spikes. For instance, legislation might focus on drawing more reinsurance capital into the state to spread risk and contain rate increases.

Special Legislative Sessions and Reforms

In response to the volatile insurance market, Florida has convened special legislative sessions, such as one in May 2022, where lawmakers passed significant reforms. Governor Ron DeSantis signed these bills aimed at optimizing insurer accountability and bolstering consumer protections.

These sessions often result in new regulations to improve the resilience of the insurance sector, directly impacting the rates and coverage options for property owners.

Impact of Legal Challenges and Litigation

Litigation and legal challenges also press upon the property insurance sphere. Lawsuits, often citing fraud or other irregularities, can lead the state to further adjust regulations. The Insurance Information Institute reports these legal proceedings as essential factors that can drive up costs due to increased liabilities, influencing the market’s dynamics and ultimately affecting insurance premiums for property owners.

Insurance Claims and Litigation Issues

Florida’s real estate market is uniquely influenced by its insurance landscape, which is dominated by a high volume of claims, particularly due to hurricane impact, and exacerbated by issues surrounding litigation.

Rising Insurance Claims and Hurricane Impact

Hurricane Season:

- Frequency: Hurricanes hit Florida more often than any other state.

- Claims: These weather events lead to a surge in insurance claims as property owners seek to repair hurricane damages.

Insurers face the challenge of addressing these claims while remaining financially viable. The concentration of claims after hurricanes often leads to insurers reassessing their coverage terms and sometimes increasing premiums, which affects property owners.

Fraudulent Claims and Excessive Litigation

Exploitation of Assignment of Benefits (AOB):

- Strategy: Individuals use AOB to transfer their insurance claim rights to third parties.

- Outcome: This has led to excessive litigation, often uncorrelated with the actual damage.

Impact of Litigation on the Real Estate Market:

- Insurers are increasingly cautious, affecting their willingness to insure properties.

- Mitigation: The state has enacted reforms to address this, such as eliminating one-way attorney fees, which previously incentivized lawsuits by allowing attorneys to collect large fees from insurance companies.

Property insurance issues in Florida remain a critical factor impacting not only homeowners but also the broader real estate sector.

Industry and Market Dynamics

The Florida property insurance market is undergoing significant stress with insurers facing solvency issues and market exits, impacting the landscape of coverage providers within the state.

Insurer Solvency and Market Exit

Insolvent Insurers: A number of insurance companies have declared insolvency, leading to a reduction in consumer choice and increased pressure on remaining insurers’ financial stability. This trend indicates a growing concern regarding the stability of property insurers in Florida.

Market Departures: Insurers, including major ones like Farmers Insurance, are reconsidering their presence in Florida, with some opting to leave the market altogether. This shift is often due to substantial underwriting losses and regulatory challenges.

Citizens Property Insurance Corp’s Role

State-Backed Insurer: Citizens Property Insurance Corp, serving as the insurer of last resort, has seen a swell in policy count as other insurers falter. This growth increases Citizens’ exposure and puts pressure on its reserves.

Policyholder Impact: As the private market contracts, more policyholders are driven to Citizens Property Insurance Corp, even though it typically offers rates at least 15% higher than the private market.

Shift Toward the Private Market

Private Market Attraction: Despite the challenges, there is a move toward the private insurance market. Insurers are recalibrating rates and policy terms to mitigate risks and maintain viability.

Novel Strategies: Private insurance companies are employing new strategies to sustain operations, though they continue to grapple with losses and the need to fortify their reserves against future claims.

Economic Factors Affecting the Insurance Sector

The insurance sector in Florida is uniquely challenged by a variety of economic factors, which include rising inflation rates and the perennial threat of natural disasters, that heavily influence insurance costs.

Inflation and Its Influence on Insurance Costs

Inflation affects the property insurance sector as it increases the replacement costs of homes and possessions. For insurers in Florida, this translates into higher claims payouts when disasters strike. Additionally, operational costs for insurance companies escalate in tandem with inflation, often leading to increased insurance premiums for homeowners.

Comparatively, the rate of inflation nationwide can also affect the insurance market as it influences the economic stability of insurers and their ability to underwrite policies.

Natural Disasters and Flood Insurance Demand

Florida’s propensity for natural disasters, particularly during the hurricane season, significantly drives the demand for comprehensive property insurance, including flood coverage. As the state encounters hurricanes, the associated costs of damage can strain insurers, resulting in a push towards higher premiums and more restrictive policy terms.

For example, the recent hike in demand for flood insurance is a direct response to the increased frequency and intensity of storms that Florida has experienced compared to other states like Georgia, which typically see less severe weather-related events.

Comparative Analysis with Other States

The Florida insurance market is facing considerable strain as insurance lawsuits remain disproportionately high compared to other states. This litigation prevalence, combined with high rates of natural disaster-related claims, poses a unique challenge that is not seen at the same level in other states such as Georgia. Consequently, these factors lead to a struggling market with steep insurance costs in Florida.

By evaluating economic factors such as inflation, natural disaster damage, and comparative analysis with other states, it becomes evident that these forces collectively shape the insurance landscape in Florida. This impacts not only the affordability and availability of insurance products but also the overall real estate market within the state.

Future Projections and Industry Outlook

The Florida real estate market is closely influenced by the state’s property insurance sector, with implications for stability, growth, and the introduction of new policies.

Predicting Stability and Growth in the Florida Market

Florida’s property insurance market has experienced significant turbulence, which has inevitably impacted the real estate sector. Looking ahead, the industry seeks a state of stability to foster confidence among property owners and investors. This stability is forecasted to be a catalyst for growth, as insurers adapt to new climate realities and legal frameworks. Insurance companies are under scrutiny to manage risks effectively while maintaining affordability for policyholders.

Challenges and Opportunities for New Policies

The high incidence of litigation and associated costs in Florida necessitates innovative policy reform to drive down costs for the benefit of all stakeholders. Opportunities lie in the implementation of effective legislative measures aimed at reducing the financial burden on insurance companies from excessive legal fees, which can, in turn, secure lower premiums for property owners. New policies and reforms are expected to focus on:

- Enhanced risk assessment techniques to better predict claim costs.

- Stricter building codes to mitigate damage from natural disasters.

- Incentives for roof replacements and other loss-prevention measures.

Such strategic policy changes could encourage new players to enter the market and increase competition, potentially leading to more favorable conditions for the real estate market overall.

Buying or Selling?

Based on the most recent data, the current state of the residential market is changing fast. Whether you are a first-time buyer or a seasoned home seller, you can relying on our expertise and guidance when making one of the biggest financial decisions of your lives.

With more than 25 years in business and over 2,000 successful transactions, we have the knowledge and experience to produce results for our clients. We take a highly methodical and deliberate approach and have specific strategies to help get the best value during the transaction.

To learn more about how we help our clients, please visit our web site or contact us via email at info@quantumcos.com.