The National Association of Realtors indicated that existing US home sales have now fallen for ten straight months which is the longest streak of sales declines since 1999. Individual sales transactions were down 35.4% year-over-year and 7.7% month-over-month to a seasonally adjusted annual rate of 4.09 million units.

According to Lawrence Yun, NAR’s chief economist, “In essence, THE RESIDENTIAL REAL ESTATE MARKET WAS FROZEN IN NOVEMBER, resembling the sales activity seen during the COVID-19 economic lockdowns in 2020,”. He further indicated, “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. Plus, available housing inventory remains near historic lows.”

Median existing home prices across all property types continue to rise. As of the end of November 2022, the median price was up 3.5% (year-over-year) to $370,700. This marks 129 consecutive months of year-over-year median home price increases which is the longest-running streak on record.

Housing inventory declined for the second third month to 1.14 million units. Based on the current pace of sales, there is a 3.3-month supply of homes on the market at this time.

The average marketing time for November 2022 was 24 days, up from 18 as of November 2021 and 21 days from the prior month.

The Florida Housing Market

During the month of November 2022, the housing market in the state of Florida has more inventory and higher median prices as compared to a year ago.

Dr. Brad O’Connor, Chief Economist for the Florida Realtors, indicated that interest rates continue to adversely impact the market. He stated, “Here in Florida, we could already see that conditions were worsening in response to the rise in rates above 6% in October’s housing market data. Based on those figures, it’s not surprising that the newly released November figures for closed sales from Florida Realtors exhibit similar declines – and we should probably expect similar declines in closed sales in December, as well, given that rates were at their recent peak near 7% for much of November, when many of the homes scheduled to close in December were going under contract.

Inventory across Florida continues to improve, up 105.2% for single-family homes and 47.4% for condominiums & townhome units.

Based on the current rate of home sales, there is a 2.8-month supply of inventory currently available as of the end of November.

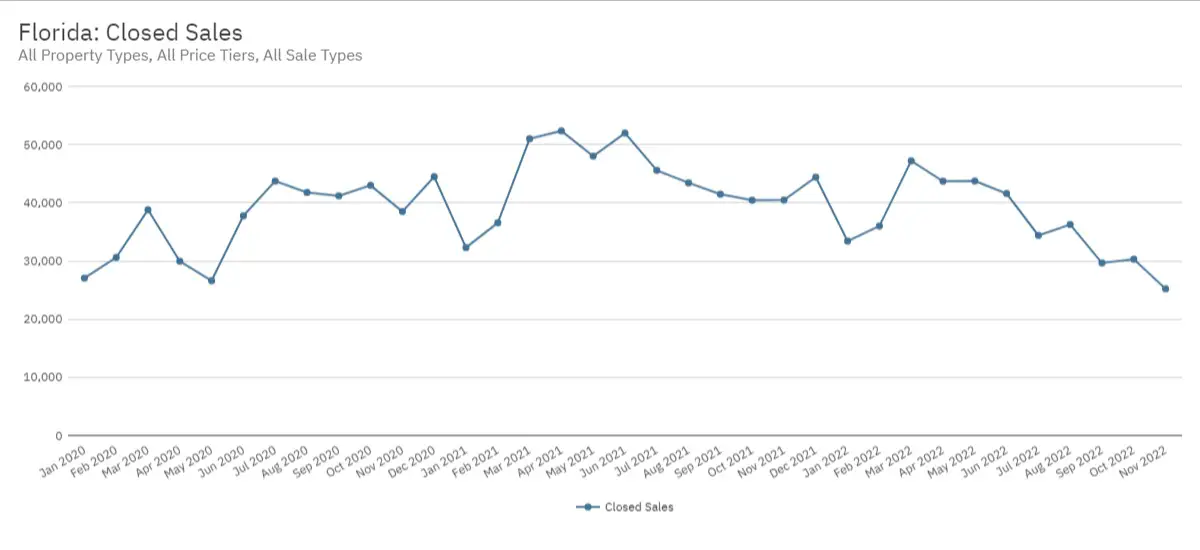

Closed Sales – November 2022

The number of closed sales transactions within the state of Florida has declined (year-over-year) for the last 11 straight months. As of November 2022, the number of individual closed sales declined by 37.71% to 25,210 transactions.

Closed Sales – Month by Month

| Month | Closed Sales | % Change YOY |

| Nov 2022 | 25,210 | -37.7% |

| Oct 2022 | 30,298 | -25.1% |

| Sept 2022 | 29,654 | -28.5% |

| Aug 2022 | 36,263 | -16.5% |

| July 2022 | 34,389 | -24.6% |

| June 2022 | 41,594 | -20.0% |

| May 2022 | 43,747 | -8.9% |

| Apr 2022 | 43,710 | -16.5% |

| Mar 2022 | 47,203 | -7.5% |

| Feb 2022 | 36,006 | -1.5% |

| Jan 2022 | 33,422 | 3.5% |

| Dec 2021 | 44,392 | -0.2% |

| Nov 2021 | 40,472 | 5.1% |

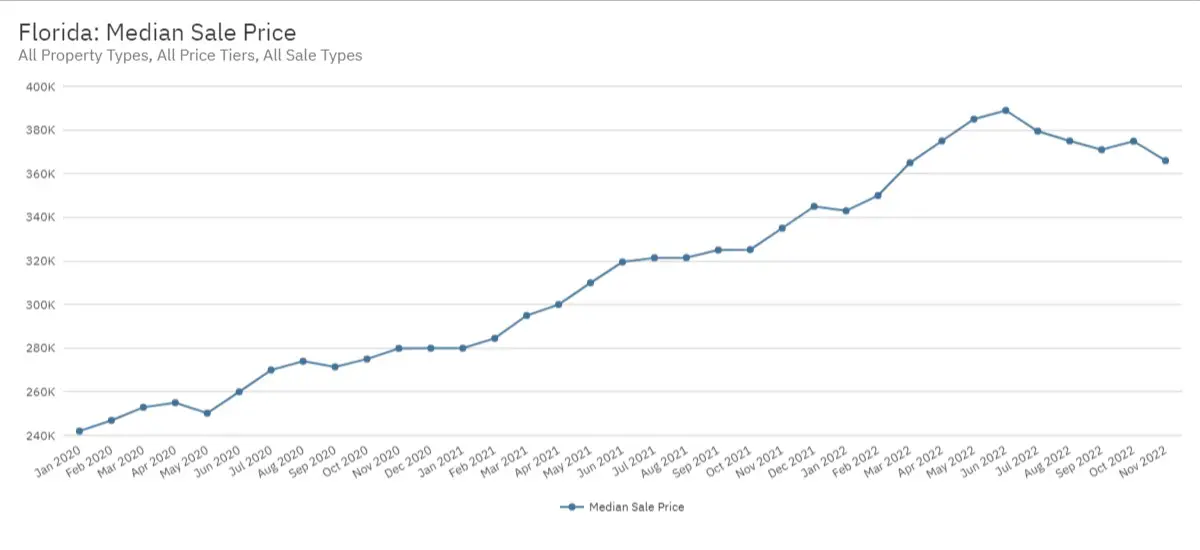

Median Sales Prices – November 2022

Median sale prices continue to exceed their year-over-year averages and increased on a month-over-month basis during the past month. During the month of November 2022, the median sale price across all property types was $365,990, up 9.3% year-over-year but down slightly from $388,990 observed in June 2022.

It does appear that a downward trend is in place.

Median Price – Month by Month

| Month | Median Price | % Change YOY |

| Nov 2022 | $365,990 | 9.3% |

| Oct 2022 | $374,900 | 15.3% |

| Sept 2022 | $370,990 | 14.2% |

| Aug 2022 | $375,000 | 16.6% |

| July 2022 | $379,500 | 18.1% |

| June 2022 | $388,990 | 21.7% |

| May 2022 | $385,000 | 24.2% |

| Apr 2022 | $375,000 | 25.0% |

| Mar 2022 | $365,000 | 23.7% |

| Feb 2022 | $350,000 | 23.0% |

| Jan 2022 | $343,000 | 22.5% |

| Dec 2021 | $345,000 | 23.2% |

| Nov 2021 | $335,000 | 19.7% |

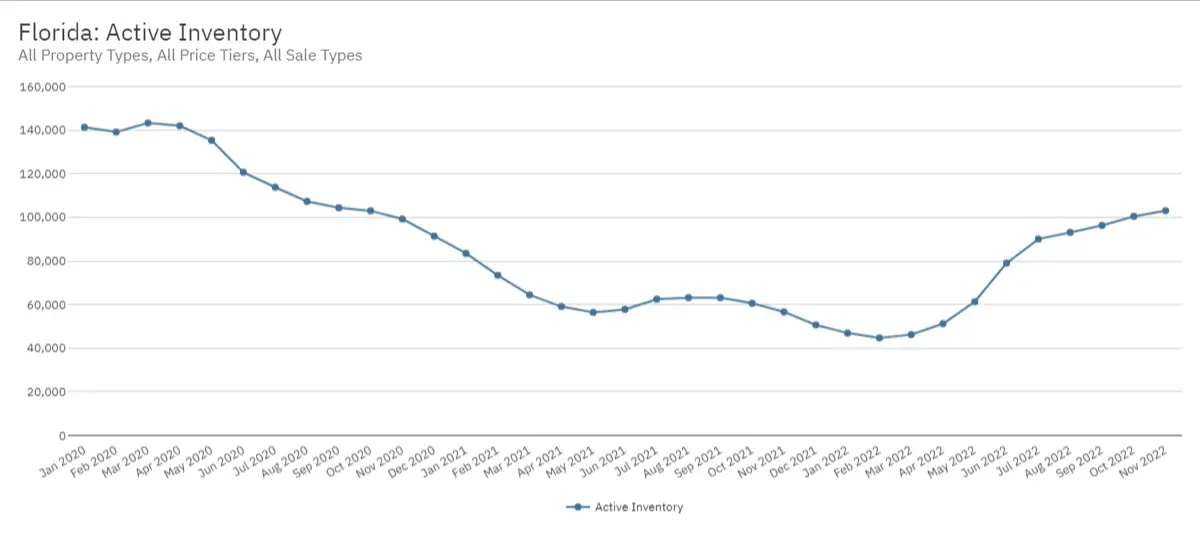

Active Inventory – November 2022

Active inventory across all property types continues to improve throughout the state. For the month November 2022, inventory is up 81.8% year-over-year to 103,016 units. This represents an increase of more than 50,000 units from the 46,247 active homes on the market as of the end of January 2022.

Active Inventory – Month by Month

| Month | Active Inventory | % Change YOY |

| Nov 2022 | 103,016 | 81.8% |

| Oct 2022 | 100,428 | 65.7% |

| Sept 2022 | 96,277 | 52.5% |

| Aug 2022 | 93,101 | 47.4% |

| July 2022 | 90,022 | 44.1% |

| June 2022 | 79,015 | 36.7% |

| May 2022 | 61,318 | 8.8% |

| Apr 2022 | 51,234 | -13.3% |

| Mar 2022 | 46,247 | -28.2% |

| Feb 2022 | 44,715 | -39.1% |

| Jan 2022 | 46,944 | -43.8% |

| Dec 2021 | 50,688 | -44.5% |

| Nov 2021 | 56,659 | -42.9% |

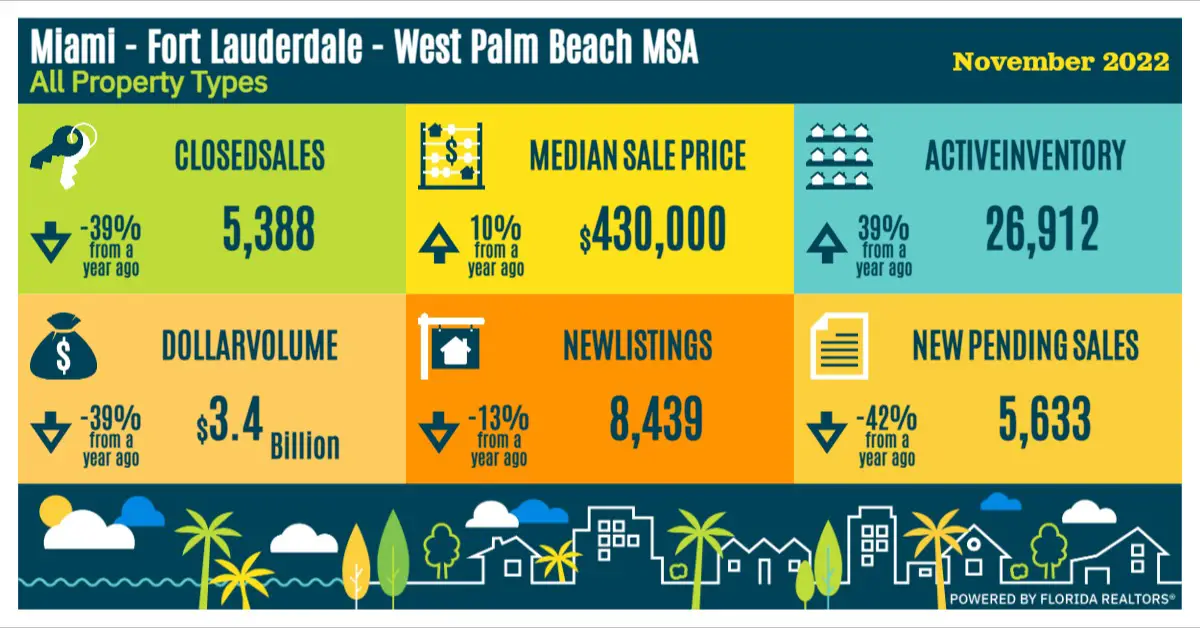

The South Florida Housing Market

The South Florida existing-home market has continued its trend of lower overall sales. Closed sales during November 2022 were down 39% year-over-year to 5,388 units. The overall dollar volume also declined by 39% to $3.4 billion.

The median home price across all property types for November 2022 increased by 10% to $430,000 year-over-year.

Inventory improved with approximately 27,000 homes across all property types available for sale within South Florida. New listings across the tri-county area were down by 13% to 8,439.

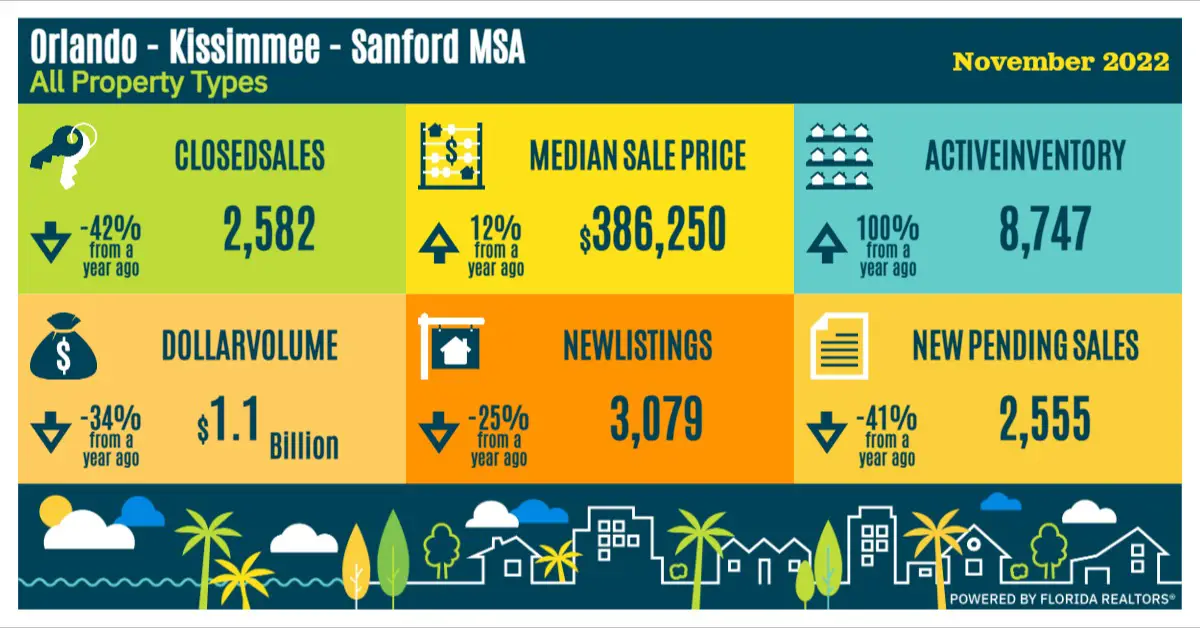

The Greater Orlando Housing Market

The Orlando – Kissimmee – Sanford existing home market continued its slowdown in sales during the month of November 2022. Closed sales of 2,582 were down 42% year-over-year along with the overall dollar volume which was down by 34% to $1.1 billion.

The median home price across all property types increased by 12% to $386,250 year-over-year.

Inventory levels continued to improve with 8,747 homes across all property types available for sale, up 100% from a year ago. New listings across the metro area were down by 25% to 3,079 units while new pending sales are down by 41% to 2,555 units.

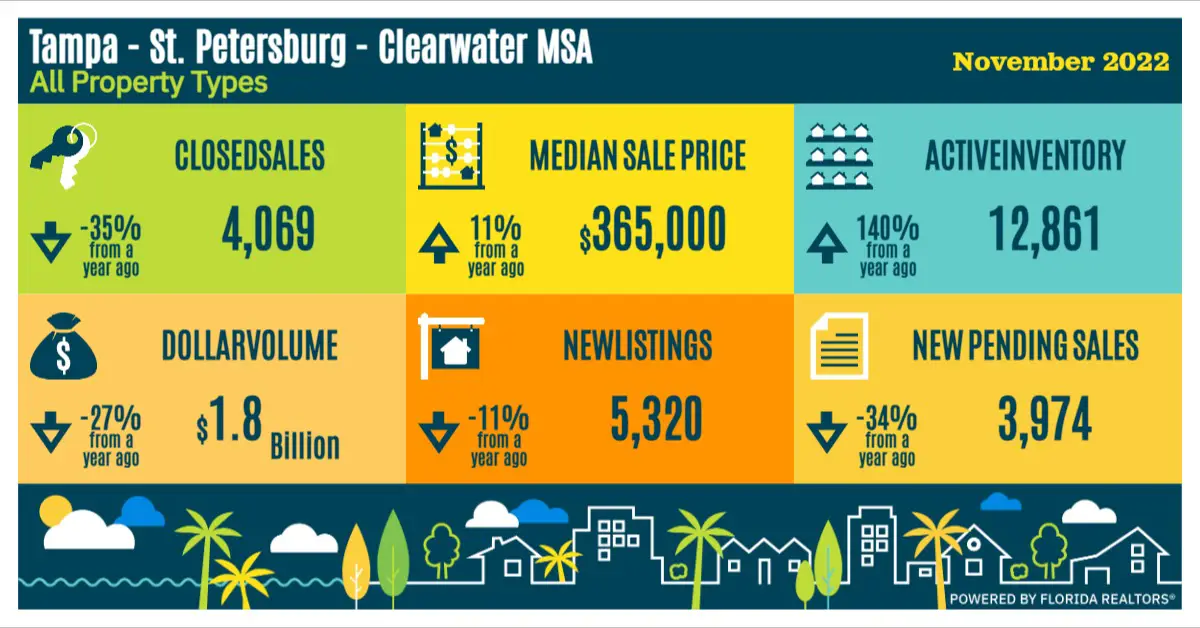

The Tampa Bay Housing Market

The Tampa – St. Petersburg – Clearwater MSA continued it’s downward trend. Existing-home sales were down 35% year-over-year to 4,069 units while dollar volume was also down by 27% to $1.8 billion.

The median home price across all property types for November 2022 increased by 11% to $365,000 year-over-year.

Inventory levels have improved by a staggering 140% (year-over-year) with 12,861 homes across all property types available for sale. New listings across the metro area were down 11% while new pending sales were down by 34% to 3,974 units.

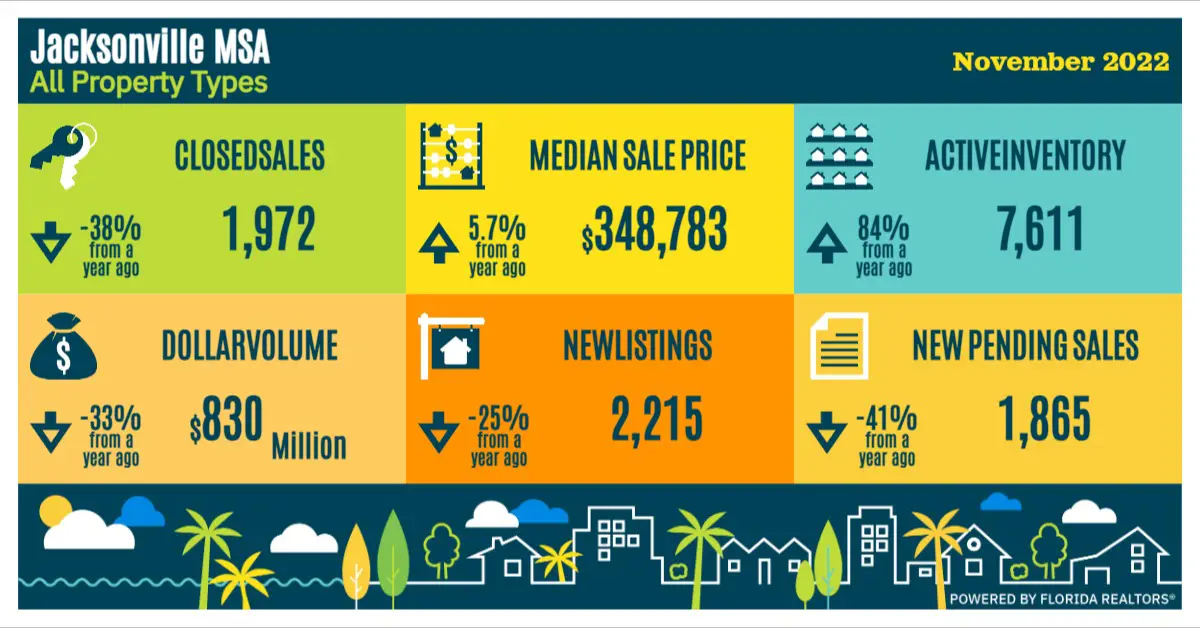

The Greater Jacksonville Housing Market

During the month of November, the greater Jacksonville housing market continued to experience slower activity with respect to home sale transactions. Closed sales of 1,972 were down 38% year-over-year and the overall dollar volume was also down by 33% to $830 million.

Prices across all property types continue to rise by double digits – the median home price increased by 5.7% to $348,783 year-over-year.

Inventory continues to improve with approximately 7,611 homes across all property types available for sale within the greater Jacksonville area, a 84% increase year-over-year. New listings were down 25% to 2,215 homes while new pending sales declined by 41% to 1,865 homes.

Are you thinking of selling?

Based on the most recent data, the current state of the residential market is changing fast. If you are a homeowner and are considering selling your personal residence, vacation home or investment property, now may be the perfect time to do so while prices are still strong.

Our team has assisted sellers not only throughout the state of Florida, but in most major markets nationwide. We take a highly methodical and deliberate approach when working with or clients and have specific strategies to help get the best value for the property.

To learn more about how we help our clients get the best possible price for their property, visiting our web site or contact us at info@quantumcos.com.