According market data published by the National Association of Realtors (NAR), the median existing US home sale prices continued their decline during the month of March 2023. Prices were down 0.9% year-over-year from $379,300 to $375,700 across all housing types. Prices increased in the Midwest Northeast and Southern parts of the country but declined in the West.

Per Lawrence Yun, NAR’s chief economist, “Home prices continue to rise in regions where jobs are being added and housing is relatively affordable”. He further stated, “However, the more expensive areas of the country are adjusting to lower prices.”

Sale transactions also declined, retreating by 2.4% from February 2023. However on a year-over-year basis, sales transactions were down 22% to a seasonally adjusted annual rate of 4.44 million units.

Existing home inventory was up 5.4% year-over-year to 930,000 units and based on the current pace of sales, there is a 2.6-month supply of homes on the market at this time. The average marketing time for the month was 29 days, up from 17 as of March 2022 but down from 34 days from the prior month.

Investors and vacation / second home buyers, purchased 17% of all homes sold in March, down slightly from 18% in March 2022.

The Florida Housing Market

Closed sale transactions across the state of Florida continue to decline on a year-over-year basis. During the month of February 2023 sale transactions across all property types are down by 17.3% (year-over-year). However, the number of closed sales improved considerably from that realized during the prior month.

Median home prices appear to level since mid-2022 but improved by 2.7% over that realized in March 2022. Inventory across Florida continues to improve, up 110.6% across all property types.

Based on the current rate of home sales, there is a 2.9 month supply of inventory currently available as of the end of March.

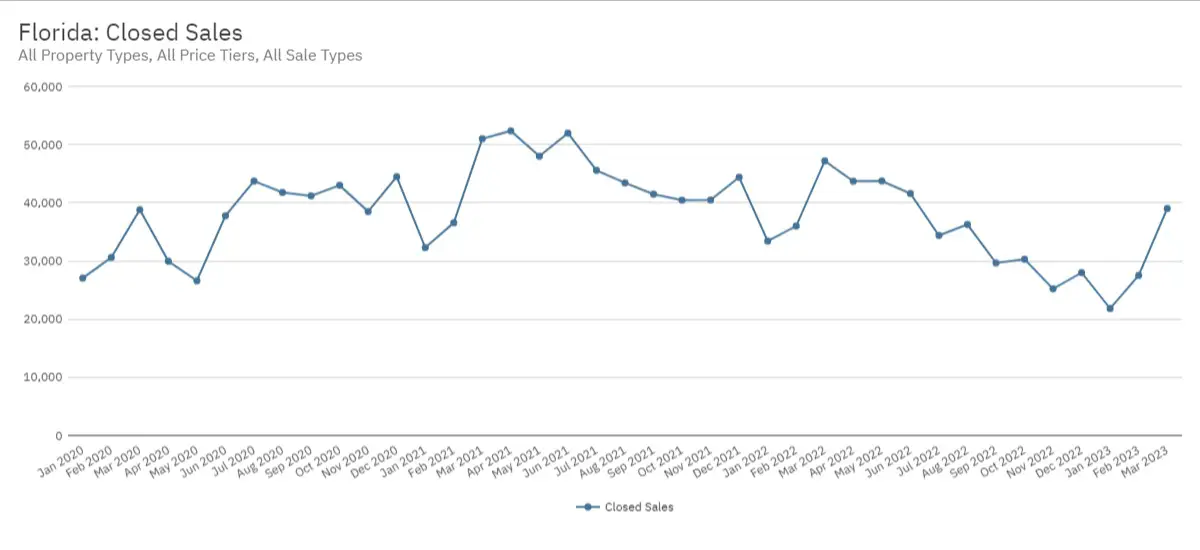

Closed Sales – March 2023

The number of closed sales transactions within the state of Florida has declined (year-over-year) for the last year. As of March 2023, the number of individual closed sales declined by 17.3% to 39,016 transactions.

Closed Sales – Month by Month

| Month | Closed Sales | % Change YOY |

| Mar 2022 | 39,016 | -17.3% |

| Feb 2023 | 27,514 | -23.6% |

| Jan 2023 | 21,825 | -34.7% |

| Dec 2022 | 27,994 | -36.9% |

| Nov 2022 | 25,210 | -37.7% |

| Oct 2022 | 30,298 | -25.1% |

| Sept 2022 | 29,654 | -28.5% |

| Aug 2022 | 36,263 | -16.5% |

| July 2022 | 34,389 | -24.6% |

| June 2022 | 41,594 | -20.0% |

| May 2022 | 43,747 | -8.9% |

| Apr 2022 | 43,710 | -16.5% |

| Mar 2022 | 47,203 | -7.5% |

| Feb 2022 | 36,006 | -1.5% |

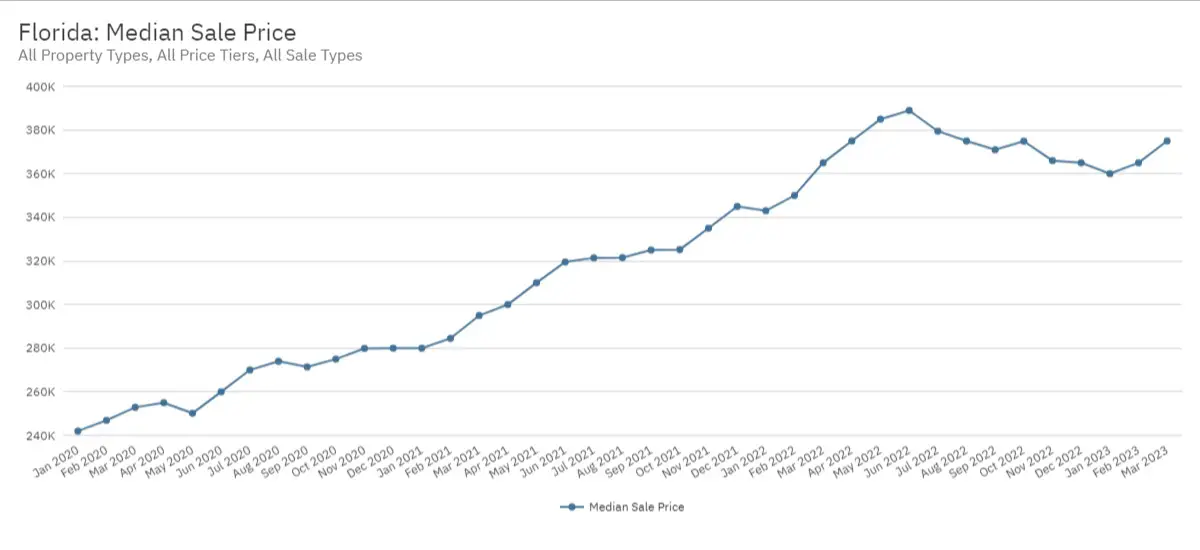

Median Sales Prices – March 2023

Median sale prices continue to exceed their year-over-year averages but continue to decline since peaking in June 2022. During the month of March 2023, the median sale price across all property types was $375,000, up 2.7% year-over-year but down from the peak ($388,990).

The state is seeing a small rising trend during the first quarter of this year.

Median Price – Month by Month

| Month | Median Price | % Change YOY |

| Mar 2022 | $375,000 | 2.7% |

| Feb 2023 | $365,000 | 4.3% |

| Jan 2023 | $360,000 | 5.0% |

| Dec 2022 | $365,000 | 5.8% |

| Nov 2022 | $365,990 | 9.3% |

| Oct 2022 | $374,900 | 15.3% |

| Sept 2022 | $370,990 | 14.2% |

| Aug 2022 | $375,000 | 16.6% |

| July 2022 | $379,500 | 18.1% |

| June 2022 | $388,990 | 21.7% |

| May 2022 | $385,000 | 24.2% |

| Apr 2022 | $375,000 | 25.0% |

| Mar 2022 | $365,000 | 23.7% |

| Feb 2022 | $350,000 | 23.0% |

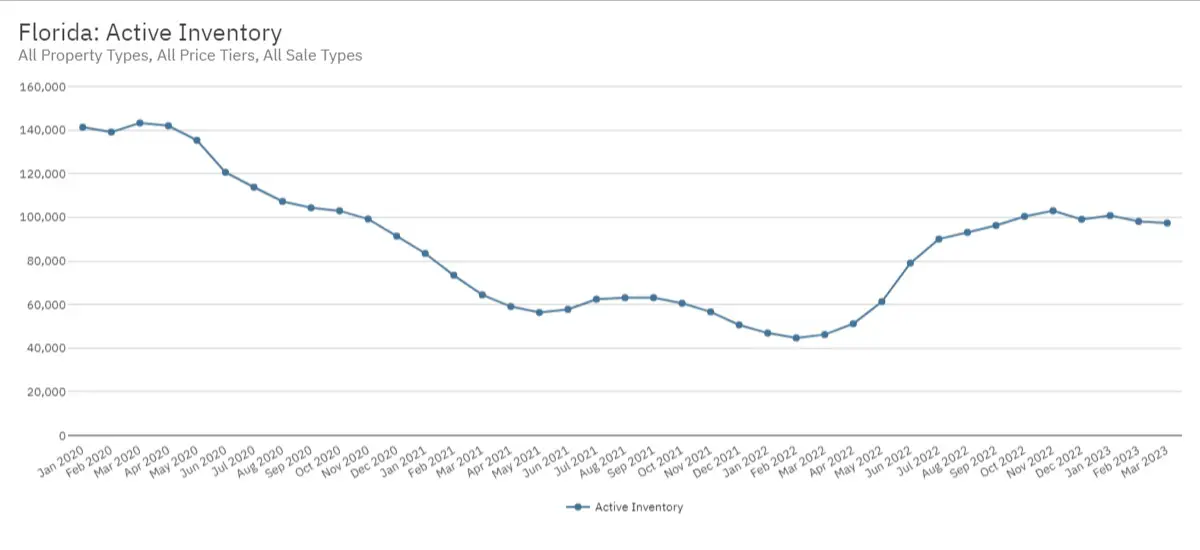

Active Inventory – March 2023

Active inventory across all property types continues to improve throughout the state. For the month March 2023, inventory is up by 110.6% year-over-year to 97,392 units. This represents an increase of more than 50,000 units from the 46,944 active homes on the market as of the end of January 2022.

Active Inventory – Month by Month

| Month | Active Inventory | % Change YOY |

| Mar 2022 | 97,392 | 110.6% |

| Feb 2023 | 98,073 | 119.3% |

| Jan 2023 | 100,798 | 114.7% |

| Dec 2022 | 99,084 | 95.5% |

| Nov 2022 | 103,016 | 81.8% |

| Oct 2022 | 100,428 | 65.7% |

| Sept 2022 | 96,277 | 52.5% |

| Aug 2022 | 93,101 | 47.4% |

| July 2022 | 90,022 | 44.1% |

| June 2022 | 79,015 | 36.7% |

| May 2022 | 61,318 | 8.8% |

| Apr 2022 | 51,234 | -13.3% |

| Mar 2022 | 46,247 | -28.2% |

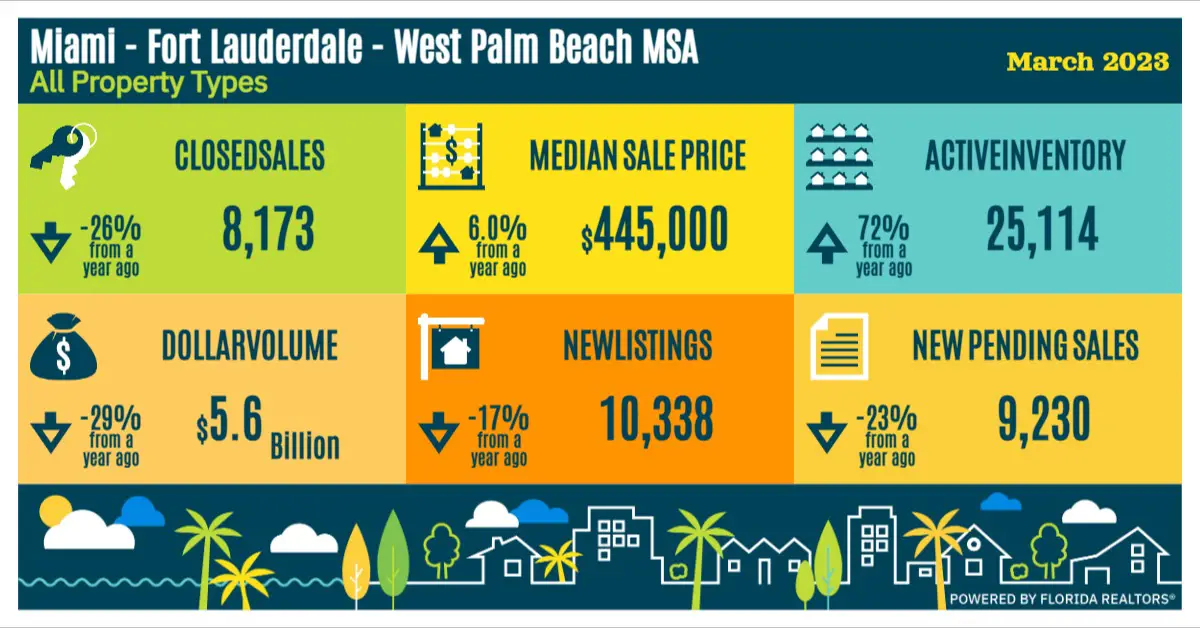

The South Florida Housing Market

The South Florida existing-home market continues the trending of lower overall home sales. Closed sales during the month were down 26% year-over-year to 8,173 units. The overall dollar volume also declined by 29% to $5.6 billion.

The median home price across all property types for March 2023 increased by 6% to $445,000 year-over-year.

Inventory improved with approximately 25,000 homes across all property types available for sale within South Florida. New listings across the tri-county area were down by 17% to 910,338.

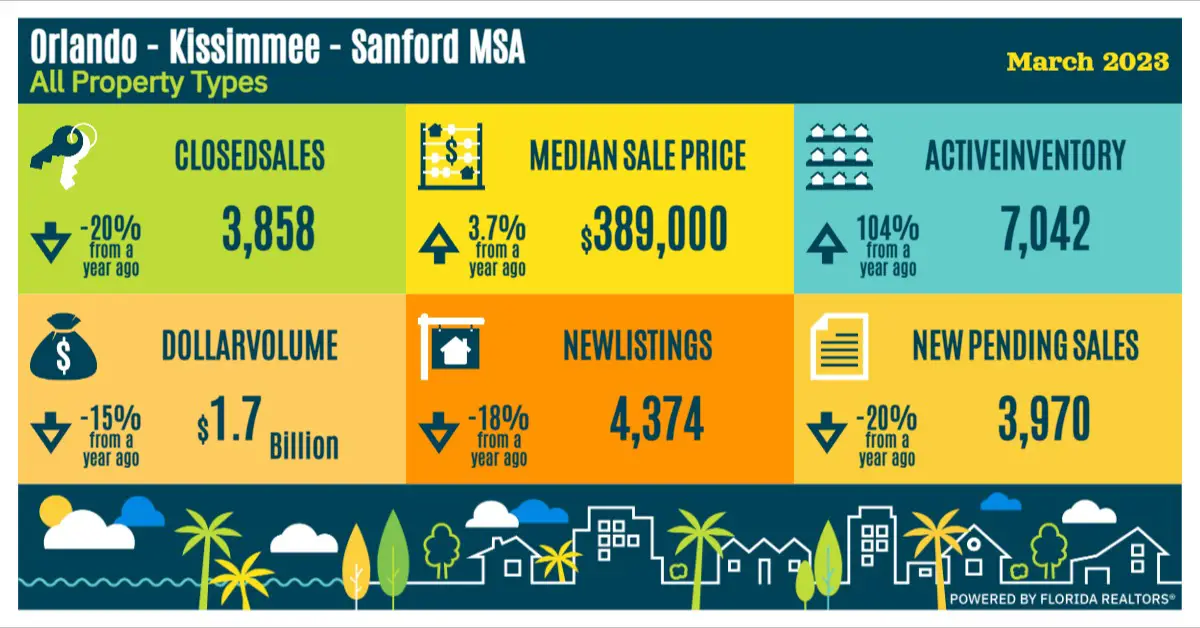

The Greater Orlando Housing Market

The Orlando – Kissimmee – Sanford existing home market continued its trend of a slowdown in sales. Closed sales of 3,858 during the month of March were down 20% year-over-year along with the overall dollar volume which was down by 15% to $1.7 billion.

The median home price across all property types increased by 3.9% to $389,000 year-over-year.

Inventory levels continued to improve with 7,042 homes across all property types available for sale, up 104% from a year ago. New listings across the metro area were down by 18% to 4,374 units while new pending sales are down by 20% to 3,970 units.

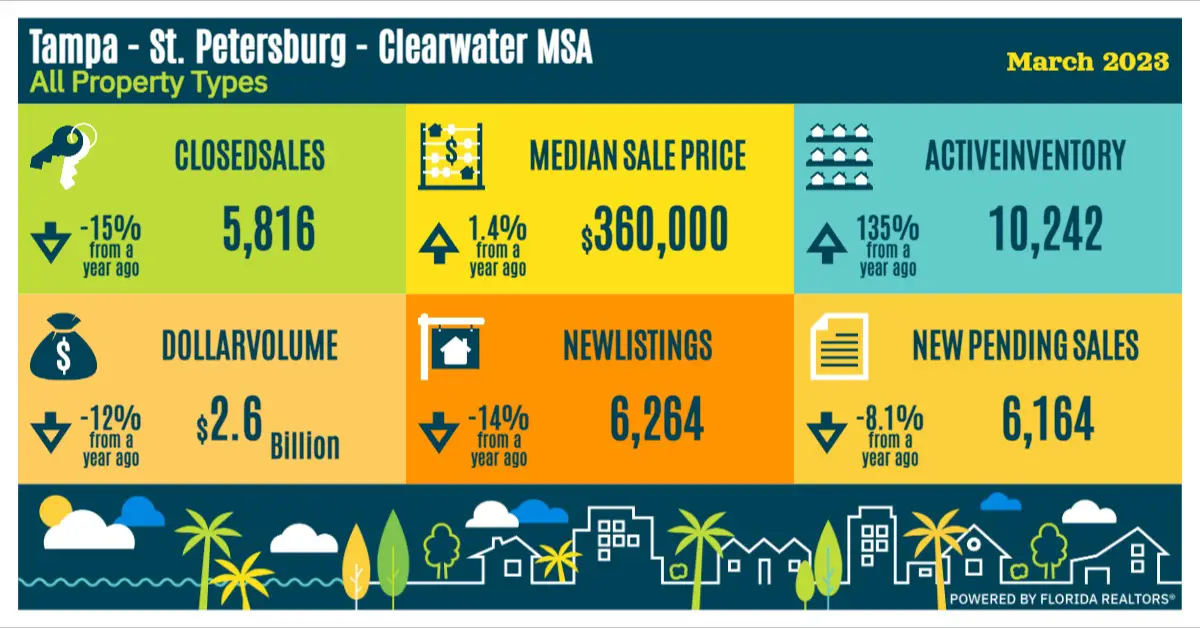

The Tampa Bay Housing Market

The Tampa – St. Petersburg – Clearwater MSA also continued it’s downward trend with respect to sale transactions. Existing-home sales were down 15% year-over-year to 5,816 units while dollar volume was also down by 12% to $2.6 billion.

The median home price across all property types for March 2023 increased by 1.4% to $360,000 year-over-year.

Inventory levels have improved significantly, increasing 135% (year-over-year) with 10,242 homes across all property types available for sale. New listings across the metro area were down by 14% while new pending sales were down by 8.1% to 6,164 units.

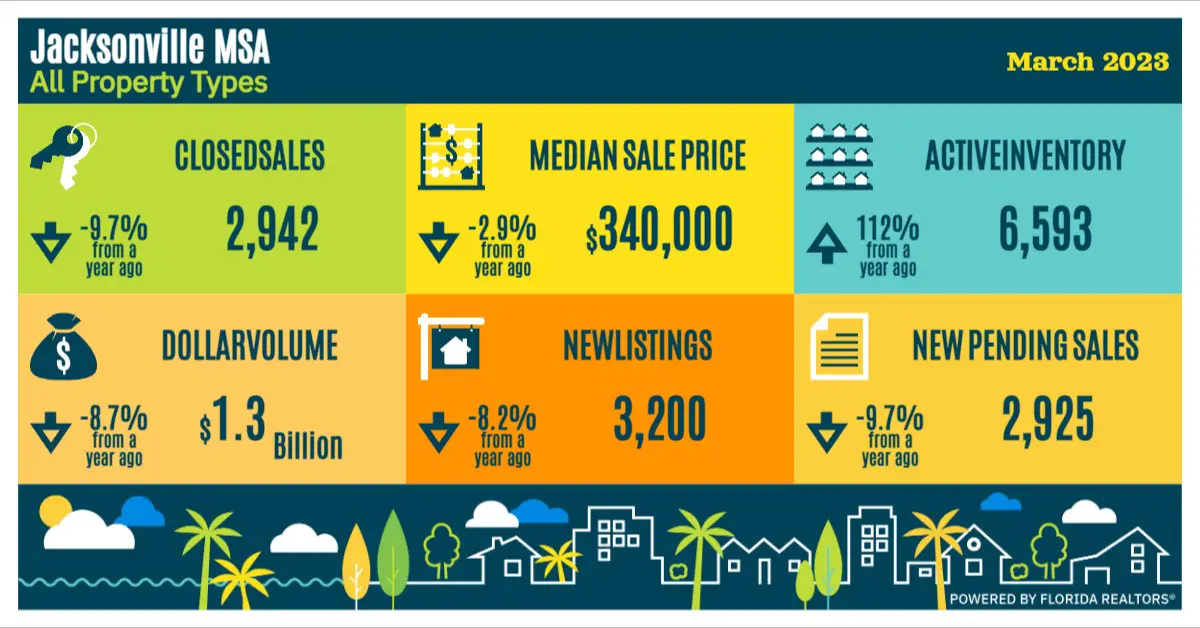

The Greater Jacksonville Housing Market

During the month of March, the greater Jacksonville housing market continued to experience slower activity with respect to home sale transactions. Closed sales of 2,942 were down 9.7% year-over-year and the overall dollar volume was also down by 8.7% to $1.3 billion.

Prices across all property types decline with the median home price declining by 2.9% year-over-year to $340,000.

Inventory continues to improve with approximately 6,600 homes across all property types available for sale within the greater Jacksonville area, a 112% increase year-over-year. New listings were down 8.2% to 3,200 homes while new pending sales declined by 9.7% to 2,925 homes.

Are you thinking of selling?

Based on the most recent data, the current state of the residential market is changing fast. If you are a homeowner and are considering selling your personal residence, vacation home or investment property, now may be the perfect time to do so while prices are still strong.

Our team has assisted sellers not only throughout the state of Florida, but in most major markets nationwide. We take a highly methodical and deliberate approach when working with or clients and have specific strategies to help get the best value for the property.

To learn more about how we help our clients get the best possible price for their property, visiting our web site or contact us at info@quantumcos.com.